We understand that applying may feel daunting and time-consuming but we'll do everything we can to make it an enjoyable experience. Selection is mutual. It allows us to find out more about you. But it's also an opportunity for you to decide whether we’re right for you. So, ask questions, allow time to think and do your research.

Remember too, that you don't need to decide where to apply right away. Talk to us, find out more about what we do and what we can do for you. On our events page, you'll find a calendar of our upcoming law fairs, presentations and workshops. Ask us anything, and we promise to give you a straight answer. You might also find it useful to complete our free virtual internship to gain an insight into our work: www.theforage.com/linklaters.

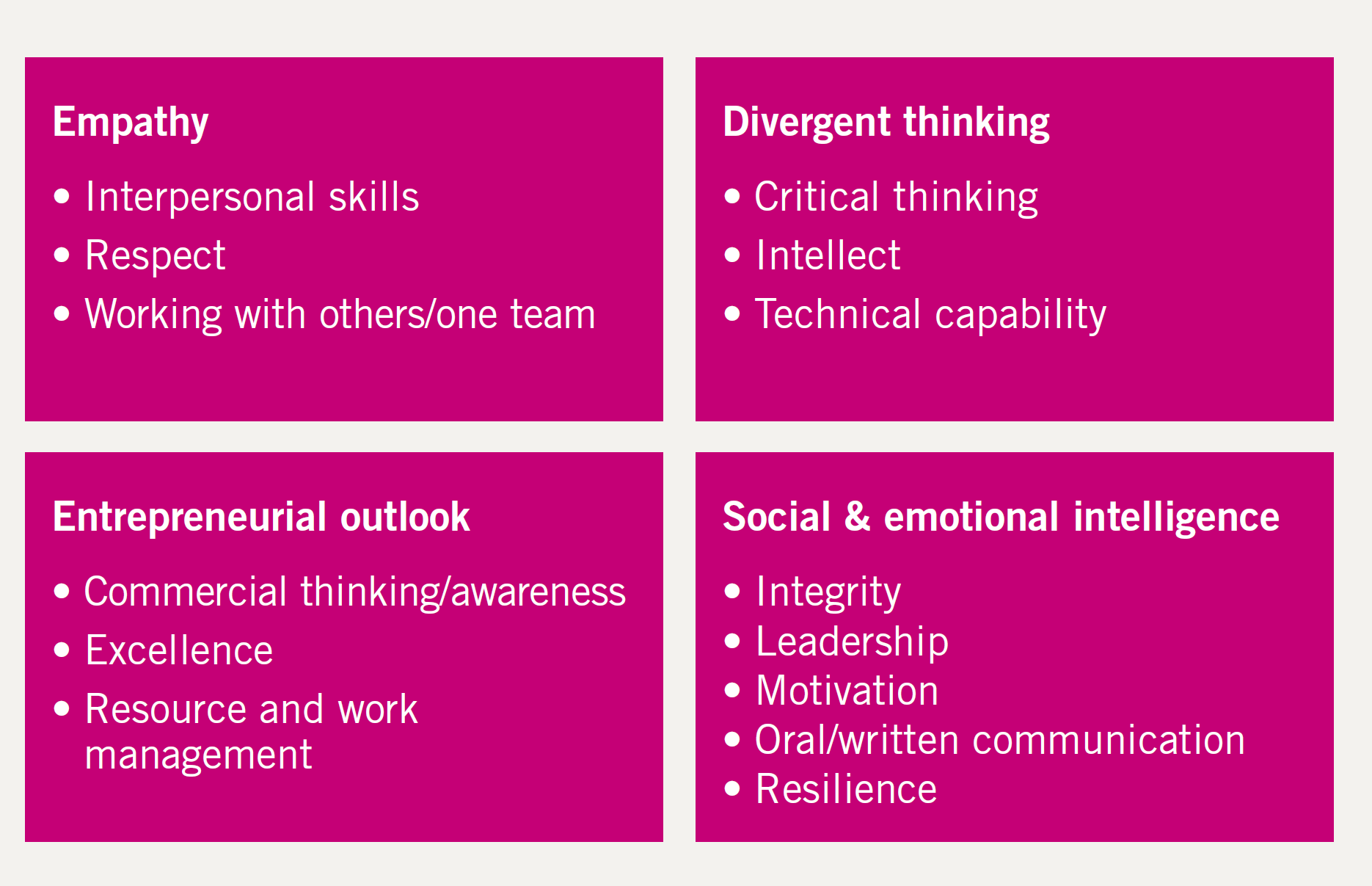

So, what are we looking for? Mindset matters. We exist to help our clients’ businesses succeed, no matter what. In a climate of great change – commercial, political and economic – that means evolving and adapting at pace to stay ahead. So, we’re looking for candidates with an agile mindset, and the ability to match. Motivated and resilient but also capable and collaborative. Consider that when completing the online assessment, taking a test or meeting us face to face.

Here is our agile mindset framework:

Contact us

If you'd like to contact a member of the Trainee Recruitment team about our application process, or require any reasonable adjustments, please email using the link below.